Something slightly different this week. I’m taking some time to respond to some other blogs. Enjoy.

1. Why do we drink beer where we drink beer? by Peter McKerry

A thought provoking post as always from Pete, which also led to some responses from Boak and Bailey and Mark Johnson amongst others. There was a lot I could relate to from Boak and Bailey, and while I couldn’t relate to “A pint of cask beer in my favourite pub ranges from £2.60 – £3.60, dependant on strength and purchase price.” from Mark’s post, he does have a point. I recently bought 7 beers from Borough Wines in Kensal Rise for £29, just over £4 a bottle. When I was at Mother Kelly’s a few week back, I was drinking halfs and two third for around £4 a serve.

I love the pub. I was a pub quiz champ and would often go to my local 2-3 times a week. Its where I met my wife. Then we had kids. Despite assertions between my wife and I that “things wouldn’t change”, they invariably do. Of course they do and its wonderful. One of the consequences is that I don’t get to the pub as often as I would like. An occasional lunchtime pint aside (Friday’s mostly), my pub visits are less spontaneous and less frequent. If my wife and I wanted to head out, we would need a babysitter at added cost. I will get out for a session every now and then where I might drink 5-6 beers, but at home I would never drink that much. Maybe a beer here and there, a few on the weekend. And yes, I do post the occasional beer (not all of them – I don’t think people want to see every time I drink a Gamma Ray) online too. Not sure how many others that drink at home more than before are recent parents too?

2. Confession Time – Which Beers are you Embarrased to Like? by Boak and Bailey

A light, fun and mischievous post. In my conversion to full beer snob, there is a number of beers that I once cherished that I have left behind. It wasn’t that long ago I was quaffing pints of Becks Vier from the local and drinking bottles of Becks in a multipack from Sainsburys. Guinness also served me well and still does. Its usually my default when there is macro’s or mediocre cask on offer. In recent times, a multipack of Dead Pony Club or Camden Hells cans has become a staple in the fridge.

3. Supermarket Craft. Various.

One of the things I do ponder is whether or not there is a craft beer bubble. Many point to the fact that craft beer only has less that 10% of the market therefore there is huge upside. While factually that might be the case, there are significant limitations to the addressable market for craft brewers and the potential upside is that craft beers maximum addressable market share might only be 25%. I’ll try and explain why below.

On-Trade

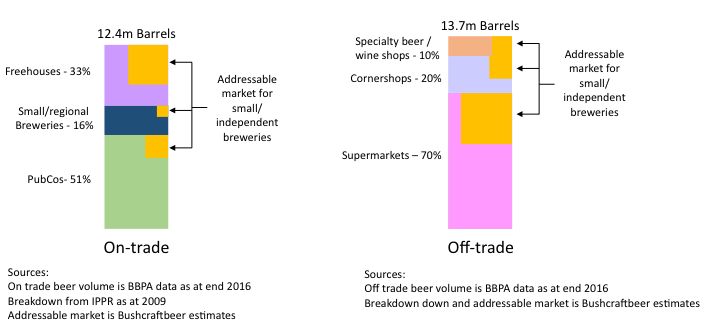

Recent BBPA figures show ontrade sales of 12.4m barrels of beer in 2016 (Barrel = 163L). This includes pubs, clubs, hotels and restaurants. I was unable to find a detailed breakdown beyond this, but let’s assume most of the beer is sold in pubs. I have used some old stats here to show the breakdown (from 2009) but directionally I am sure the are still relatively close. PubCos dominate the industry with over 50% of all pubs. It is difficult for craft breweries to get distribution into these PubCos. SIBA tries to assist with their BeerFlex scheme, but the addressable market for PubCos is small. Small and regional breweries make up 16%. Again, they will likely prioritise their own beer, therefore the addressable market is again relatively small. Freehouses are a third of all pubs, and the biggest opportunity for craft breweries. Other opportunities of course are taprooms and own premises here as you can sell 100% of your own beer at such premises.

Off-trade

Recent BBPA figures show ontrade sales of 13.7 m barrels of beer in 2016 (Barrel = 163L). Off-trade now exceeds on trade as outlined in the graph below which used BBPA figures.

What’s striking is how much on-trade has declined, rather than a huge increase from off-trade. There are around 10,000 less pubs over this timeframe which is driving the big reduction in numbers. I couldn’t find any breakdown for off-trade so have made a few assumptions: supermarkets account for 70%, corner stores 20% and speciality beer and wine shops 10%. What this crude analysis shows me is that the biggest opportunity for the craft brewer is in the supermarket. M&S you could reasonable argue have led the way with bringing craft beer to their shelves. Tesco, under Project Reset, have completely redesigned their range of craft beers, favouring US craft beer imports (Oskar Blues, Stone – albeit their german brewery, and Brooklyn), some UK brands (BrewDog, Vocation) with some regional variety) at the expense of brands such as Heineken and Carlsberg. And they are doing it in the way the know how – offering beer and cheap, cheap prices. Morrisons and Waitrose have also amended their beer range and it can’t be long before we see others such as Sainsburys and smaller players delve into craft beer. This will create opportunities for some breweries, should they wish to take it. And it is a big decision with big implications on the business model and brand of a craft brewery as well as the other routes to market.

How much impact will cheap, accessible and decent beer at supermarkets impact both other off-trade and on-trade beer sales?

Is really good beer, made and marketed well going to be enough to increase the addressable market for craft beer?

Or should craft breweries be looking at other ways to get to market?

Other opportunities of course are taprooms and own premises here as you can sell 100% of your own beer at such premises. As mentioned in a previous post, Wild Beer Cos crowdfunding campaign showed the revenue potential from their own premises. Magic Rock taproom has become such a destination, there is often lines out the door, much to Mark Johnson’s bemusement.

Time will tell.